A startup is a new business that focuses on creating unique and innovative technology solutions or services. Known for their high growth potential, startups offer numerous benefits to the economy.

This is why many countries actively encourage the creation of startups through financial incentives and simplified regulations.

In fact, in some countries, small and medium-sized businesses make up a major part of the economy.

So, if you are eager to solve a problem you are passionate about while enjoying autonomy and the potential for high returns, this guide is for you.

It offers detailed insights on how to build a startup and become part of the 10% of businesses that succeed long-term.

The path to making a startup generally looks like this:

- Research the market

- Brainstorm business concepts

- Identify a profitable idea

- Validate the idea

- Create a business plan

- Decide on financing your business

- Create a budget plan

- Secure funding

- Build a team

- Create an MVP

- Create a marketing strategy

- Launch your product

- Monitor and measure

- Pivot if you must

- Scale and grow

Voila! You are a founder.

Now, let’s get to the details.

Step 1. Research market trends

People find inspiration for startup ideas from various sources. For instance, the founders of Airbnb and Uber decided to build a startup after personally facing an inconvenience. Stripe was developed to address inefficiencies in online payments, Slack started as an internal tool within a company, and SpaceX grew from a passion.

Yet, even if you’re confident that your idea is exactly what the world needs, it won’t hurt to double-check. This step is also helpful if you don’t have a specific idea yet, as it will help you identify opportunities for a successful startup.

Here’s what to do:

- Look for emerging demands and anticipate where the market is heading;

- Understand what products and services are gaining popularity and why;

- Analyze for areas where consumer needs are not being fully met;

- Identify products and services the demand for which is fading to avoid investing in those areas.

Below are some tools that can help you obtain the insights:

- Google Trends is useful for identifying trending topics or declining interests in specific areas;

- Social media analytics (e.g., Facebook Insights, Twitter Analytics) can provide data on what topics are engaging audiences and how people interact with brands or products;

- Industry reports, such as those provided by Nielsen or Kantar, can yield deep insights into consumer trends, market segmentation, and competitive landscapes;

- Crunchbase is an excellent place to learn about successful companies in a specific industry, including their funding rounds, investors, and recent news. This can help you identify market trends and potential gaps.

Step 2. Brainstorm business concepts

As you explore possibilities, it’s time to get creative and jot down potential ideas for your startup to develop. At this stage, focus on quantity rather than quality of the ideas.

Here are some techniques to help you brainstorm effectively:

- Mind mapping: Start with a central concept and expand into sub-themes, exploring different aspects or components of an idea;

- Brainwriting: Gather a friend or a group of people whose opinions you trust and value. Have them write down their ideas on paper, then pass the paper to the next person who adds more thoughts. This method allows for quiet reflection and building on others’ ideas;

- SCAMPER: This stands for Substitute, Combine, Adapt, Modify, Put to another use, Eliminate, and Reverse. Use this checklist as prompts to think creatively about existing products or services;

- Problem-solving: Focus on specific problems faced by potential customers. Brainstorm solutions that a startup could offer.

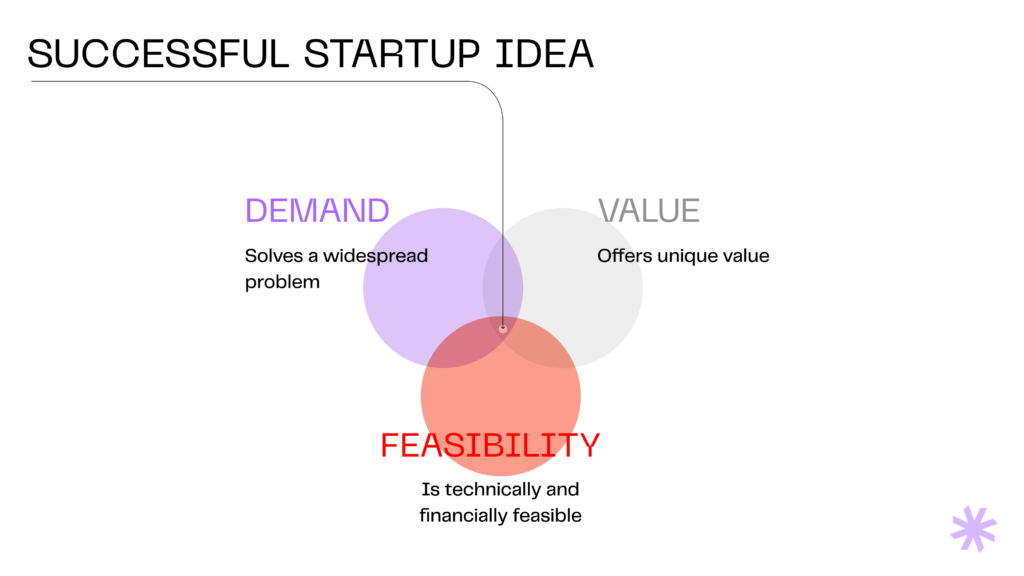

Step 3. Identify a profitable idea

After the brainstorming session, analyze the ideas. Take the promising ones and either expand on them or combine them with others to explore potential synergies or new angles.

As a rule of thumb, a successful idea should have the following characteristics:

- Solve a widespread problem

- Offer unique value

- Be technically and financially feasible

Step 4. Validate the idea

After “How to create a startup?” the next big question is, “Will people want to buy my idea?” Validating a startup idea means checking if there is a real demand for your product or service and determining how much consumers are willing to pay.

Here’s how you can do it:

- Form core hypotheses about who your target customers are, the problems they face, and how your product or service can solve these problems;

- Gather supporting information. Use industry reports and studies to back up your hypotheses, and consider conducting surveys, interviews, and focus groups with your target audience. This will help you collect firsthand information about their needs and behaviors.

Test your idea with an MVP

Check the feasibility of your business idea, get real user feedback, and impress investors with a working product. Syndicode will help you launch quickly.

Let’s talkStep 5. Create a business plan

A formalized business plan helps you visualize how to build a startup and map out its future growth. It will help you stay aligned with your team and investors, understand the feasibility of your business model and mitigate risks. Additionally, it will guide your long-term operations, finances, and marketing strategies.

Here are the key points to include in your business plan:

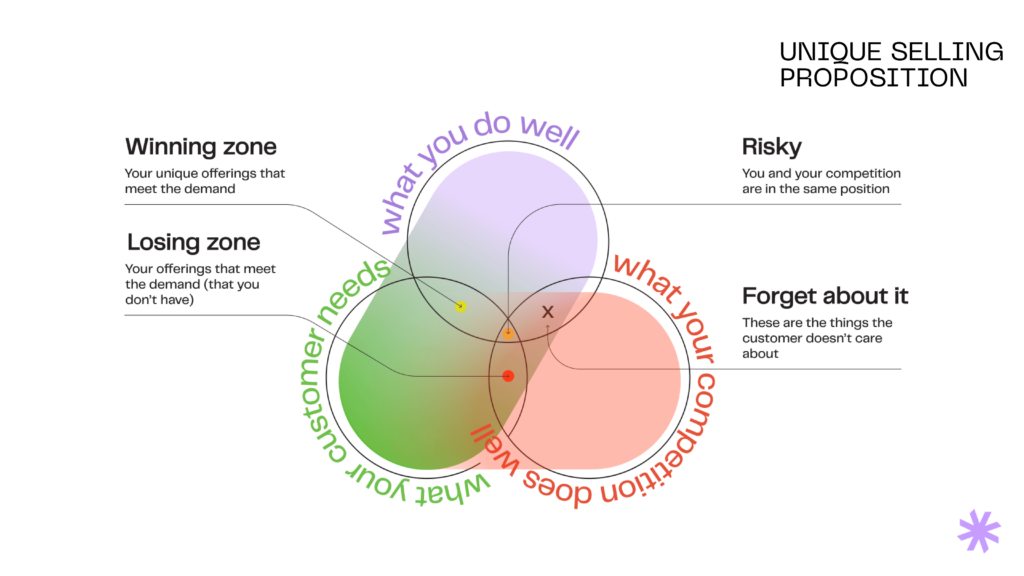

Define the target market and USP

- Select your target market. Use the insights from your market research to identify the segment(s) that align best with your business’s strengths and the unique benefits of your product or service. Consider factors such as market size, accessibility, profitability, and how well they align with your brand values;

- Analyze competitors. Learn how to build a startup from them and understand who they’re targeting and how they position themselves. Look for areas where you can clearly distinguish yourself;

- Create customer profiles or personas for your target market. Include details like typical age, income, lifestyle choices, and buying behavior;

- Clarify your unique selling proposition (USP). Identify what sets your offering apart from competitors, whether it’s product features, pricing, customer service, technology, design, or brand experience;

- Craft your message by translating the benefits of your product or service into clear advantages for customers. Consider this message as the answer to the customer’s question, “Why should I buy from you?”

Choose a monetization model

At this stage, you should have a good understanding of the typical revenue generation methods in your chosen market. However, if you’re still unsure about how to make your startup earn money, consider prototyping different models to see which one is most effective.

For instance, you can easily test both a subscription model and a one-time purchase option to collect customer feedback and determine their preferences.

| Monetization model | Description | Best for |

|---|---|---|

| Direct sales | Selling a product or service directly to consumers or businesses | Products with clear, tangible value |

| Subscription | Charging a recurring fee for continued access to a product or service | Services that offer ongoing value (digital platforms, SaaS products, membership sites) |

| Freemium | Offering a basic version of a product or service for free while charging for premium features | Software and services where the free version serves to build a user base |

| Advertising | Generating revenue through ads displayed on the platform | Products with significant traffic or user engagement |

| Affiliate marketing | Earning commissions by promoting other companies’ products or services | Content-driven websites and blogs |

| Licensing | Charging a fee for the use of the technology or intellectual property | Unique tech solutions or creative content |

| Transaction fees | Taking a cut from transactions between users on the platform | Marketplaces and fintech solutions |

Set goals

Every business needs a strategy, which essentially consists of the short-term and long-term goals you set for your startup. These goals are crucial for demonstrating your commitment to investors and for evaluating your progress.

- Setting short-term goals

Short-term goals for a startup typically focus on immediate to one-year achievements that lay the foundation for future success. They should be actionable and help build momentum.

To set effective short-term goals, identify immediate needs that must be addressed in the next 3 to 12 months. This could include launching a minimum viable product (MVP), securing initial funding, acquiring paying customers, or establishing key partnerships.

- Setting long-term goals

Long-term goals focus on where you envision your startup in several years. These goals are broader, reflecting your vision for the company’s future, including growth, market presence, and financial stability.

Examples of long-term goals might include achieving specific revenue targets, expanding to new markets, or launching new products.

To set effective long-term goals, consider your desired position in the broader industry landscape and ensure these goals align with the company’s vision and mission.

- SMART framework

An effective way to approach goal setting is to use the SMART framework, which stands for specific, measurable, achievable, relevant, and time-bound.

Choose your business structure

Your business should comply with legal requirements to function safely. We recommend consulting with local authorities to learn how to build a startup properly, as the chosen legal structure affects your taxes, liability, and management structure.

Here are the common legal structures for startups in the USA:

| Legal structure | Description | Taxes | Liability |

|---|---|---|---|

| Sole proprietorship | Single owner, the simplest form of business | Income is reported on the owner’s personal tax return; the business itself isn’t taxed separately | The owner is personally liable for all business debts and obligations |

| Partnership (general, LP, or LLP) | Two or more people own the business | No income tax. Income or losses are passed through to partners’ personal tax returns | General partnership: all partners share liability; LP: general partners are fully liable, limited partners have limited liability; LLP: liability is limited for all partners |

| Limited liability company (LLC) | Combines the flexibility of a partnership with the liability protection of a corporation | Can choose to be taxed as a sole proprietor, partnership, or corporation | Owners (members) have limited personal liability for business debts |

| Corporation (C-Corp) | Owned by shareholders, managed by a board of directors, and operated by officers | Subject to corporate income tax. Profits distributed as dividends are taxed again at the shareholders’ personal tax rate (double taxation) | Shareholders have limited liability, protecting personal assets from business debts |

| S corporation (S-Corp) | Same as C-Corps but with a limited number of shareholders | Income is taxed at individual tax rates on shareholders’ returns, not at the corporate level | Shareholders have limited liability |

Register your business

Registering your startup is a crucial step that turns your business into a legal entity. Ideally, you should register your business before you start any commercial activities, such as signing contracts, receiving payments, or issuing invoices. This ensures that all business operations are legally conducted under the business entity, providing legal protection and a proper financial record.

Here’s what registering a startup typically involves:

- Choosing a name for your startup;

- Obtaining an Employer Identification Number (EIN). This is essential for hiring employees, opening business bank accounts, and paying taxes;

- Registering your business with the state to secure the necessary licenses and permits;

- Opening a business bank account;

- Securing insurance.

Step 6. Decide on financing your startup

When you think about how to build a startup, you’ll naturally wonder where to find funding.

Start by evaluating your startup’s industry, potential for growth, and how much control you are willing to share. It often helps to combine different finding options at various stages of your business lifecycle to optimize growth and financial health.

| Funding option | Description | Advantages | Considerations |

|---|---|---|---|

| Bootstrapping | Using own savings or initial sales revenues to fund the business | Full control over business decisions, no debt or equity commitments | Growth speed is limited by the amount of personal funds or revenue |

| Friends & Family | Raising money from personal connections. Can be structured as a loan or equity in the company | Potentially easier to secure due to personal relationships, flexible terms | Can strain personal relationships if the business doesn’t perform well |

| Angel investors | Wealthy individuals provide capital for startups in exchange for convertible debt or ownership equity | Angels can additionally offer valuable advice and network access | May require equity in return, which dilutes the ownership |

| Venture capital | Professional groups that manage pooled funds from multiple investors | Large amounts of capital, strategic assistance, networking opportunities, and credibility | Significant equity requirements, high expectations for growth and returns, limited control over business decisions |

| Crowdfunding | Raising small amounts of money from a large number of people | Access to a wide pool of investors; can also serve as a marketing tool | Requires a compelling pitch and rewards, potentially high fees |

| Bank loan | Traditional loans obtained from banks or financial institutions | No equity dilution, clear terms of repayment | Requires creditworthiness, possible collateral |

| Government grants | Government funds provided to support startups, often targeting specific industries or economic goals | Non-repayable funds, no equity dilution | Highly competitive, restricted to specific sectors or purposes, may involve compliance with specific regulations |

| Accelerators & incubators | Programs that offer seed investment, mentorship, office space, and networking opportunities in exchange for equity | Provides a structured growth path, access to valuable resources, and mentorship | Competitive to get in, requires sharing equity, intense and rapid commitment to growth |

| Corporate funding | Investment from larger companies in related industries; may include direct investment or special funding programs for startups | Access to significant resources, industry expertise, and networks | May align your startup too closely with one corporate entity, limiting future opportunities or independence |

Step 7. Create a budget and financial projections

In order to plan your future activities effectively, you need to know your finances. Follow these steps to create a realistic financial plan:

- Estimate the initial costs, such as legal fees, rent, and utilities, setup costs for IT systems, product development, and marketing;

- Project operating expenses, including employee salaries and payments for outsourced services, as well as ongoing costs to keep your business operational;

- Forecast revenue. Use your market research to make an educated guess about future sales;

- Create financial statements, including the Income Statement, Balance Sheet, and Cash Flow Statement.

It’s recommended that you include a 10–20% contingency fund in your budget.

Step 8. Secure funding from investors

Securing funding is often about finding the right partners who believe in your vision as much as it is about the financials and potential return on investment. Therefore, you’ll need to prepare the following documents to demonstrate how you plan to create a startup and maximize your chances of success:

- A business plan outlining your business model, market opportunity, competitive advantage, and growth strategy;

- Financial statements and projections;

- Cap table showing the equity capitalization for your company;

- Legal documents;

- An impressive pitch that includes the problem your business solves, how your solution is unique, how you’re planning to make money, exactly how much funding you need and why, and how investors will get a return on their investment.

You’ll probably need to tailor your approach to each potential investor based on their interests and investment thesis.

Read also: How do apps make money?

Step 9. Build a team

Once you’ve determined how to build a startup, ensure that you have the right mix of skills, experience, and cultural fit. These can greatly enhance your company’s performance and innovation.

Here’s a common strategy for recruiting the right people:

- Define your needs in terms of the roles and responsibilities necessary to achieve your business objectives. Consider the skills and personality types that will complement your startup process and improve team dynamics;

- Focus on key positions that are crucial for your startup’s success, such as the Chief Technology Officer (CTO), Chief Operating Officer (COO), and Chief Marketing Officer (CMO). Each core team member should be versatile enough to take on multiple roles;

- Offer incentives. While you may not compete with large companies on salary, you can offer other benefits such as equity, flexible working conditions, and opportunities for rapid professional growth;

- Use internships and temporary roles to assess potential full-time employees;

- Outsource specialized roles. For non-core tasks like website development, consider outsourcing to a trusted software development company. This will allow your core team to focus on product development, marketing, and sales.

Outsource or keep in-house?

| In-house team | Outsourced team | |

|---|---|---|

| Pros | Full control Direct communication Hand-picked employees | Easy scaling Pay-per-use Easy to switch Global talent pool |

| Cons | Long-term recurring expenses Time-consuming Requires HR skills Limited talent pool | Risk of communication issues Security risks Less control over development |

Hire seasoned MVP developers

We’ve helped dozens of startups to launch and become profitable. Share your idea with us, and we’ll return with development suggestions and estimates.

Contact usStep 10. Create an MVP

A Minimum Viable Product (MVP) is the simplest form of a product that can be released to the market. It has just enough features to attract early adopters and validate a product concept early in the development cycle.

This approach is widely used for startup development as it saves time and resources by focusing on the core functionalities that meet customer needs without unnecessary extras.

We have a complete guide devoted to the benefits of an MVP and how to develop one. Here, we’ll outline the key steps:

- Select core features that directly address the main problem for your initial user base;

- Design and build the MVP, keeping it simple and user-friendly. The goal is to build just enough to solicit valuable feedback, not to perfect it;

- Test with real users. Use a small group of beta testers who represent your target market. Collect and analyze user behavior and feedback to understand what works and what doesn’t;

- Iterate based on feedback received, adding, modifying, or removing features;

- Prepare for scaling. Once the product concept is validated and there is clear evidence of market demand, you’re ready to optimize the MVP for larger-scale use and enhance the product features.

Step 11. Create a marketing plan

The key to creating an effective marketing strategy on a low budget is to leverage cost-effective tactics that maximize impact. Below are several ideas on how to create a startup promotion strategy on a budget:

- Content marketing

- Blogs: share insights, guidance, and industry news to attract and engage your audience;

- Videos: create simple, informative videos using tools like your smartphone or free video editing software;

- Infographics: deliver valuable information in a visually engaging way using free graphic design tools;

- Social media marketing

- Choose platforms where your target audience is most active (e.g., Instagram for younger consumers, LinkedIn for B2B);

- Post regularly and engage with followers;

- Use hashtags strategically to increase your visibility;

- Email marketing

- Build an email list by offering something of value in exchange for email addresses, such as a free ebook, webinar, or trial;

- Use email campaigns to promote your business by providing useful content and updates;

- Search Engine Optimization (SEO)

- Optimize your website and content for search engines to increase organic traffic;

- Focus on long-tail keywords that are less competitive and more specific to your offerings;

- Partnerships and networking

- Collaborate with other businesses that complement yours for co-promotions;

- Attend or participate in community events, trade shows, and industry meetups to network with potential customers and partners;

- Referral programs

- Encourage your satisfied customers to refer new clients to you. Offer incentives like discounts or free products for successful referrals;

- Public Relations (PR)

- Write press releases or articles for local media or niche blogs about your company’s launches, updates, or events;

- Engage with local community activities and sponsor events to build brand awareness;

- Guerrilla marketing

- Use unconventional, low-cost tactics designed for maximum impact in local environments—like public installations or unique, attention-grabbing events.

Steps to create an effective marketing strategy

- Define your goals, such as increasing brand awareness, generating leads, boosting customer engagements, etc.;

- Understand your audience by identifying who your customers are, what they need, and where you can reach them;

- Select appropriate strategies based on your goals and audience. Focus on those that leverage your strengths and require minimal expenditure;

- Set a budget to manage costs effectively. Allocate funds based on the potential return of each strategy;

- Plan your actions by breaking down each strategy into actionable steps. Plan content topics, schedule social media posts, and outline email sequences;

- Use tools that are free or low-cost to implement your strategies. For instance, use social media scheduling tools like Buffer, design tools like Canva, or email marketing platforms like Mailchimp;

- Measure your marketing efforts against your goals using tools like Google Analytics and social media analytics. Be prepared to adjust your strategy based on what the data tells you about what’s working and what’s not;

- Keep refining and expanding your strategies as you learn more about what works for your business and as you grow.

Step 12. Launch your product or service

This is a pivotal moment for every startup as launching a product or service establishes your brand in the marketplace. It also provides the first opportunity for the market to interact with your product, offering real-world validation of your startup’s value proposition.

For many startups, a launch is also a test of their operational capabilities. It reveals strengths and weaknesses in areas such as supply chains, customer service, fulfillment, and support systems.

Additionally, after the launch, a startup begins to generate revenue from its operations. This is crucial, as a successful launch can attract further interest from investors and stakeholders.

Here’s how to ensure a successful launch:

Steps for a successful launch of a product or service

- Make final preparations to ensure the product or service is fully ready for public use, making sure all aspects are polished and tested;

- Create a launch strategy that includes specific goals, target audiences, key messages, and communication channels;

- Execute the marketing plan using the strategies developed earlier, such as social media announcements, email campaigns, press releases, and possibly launch events;

- Set up systems to monitor the launch in terms of customer responses, media coverage, and online engagement. Have teams ready to handle customer support and feedback;

- Evaluate the success of the launch against your initial objectives. Gather insights from sales data, customer feedback, and media coverage to assess what worked well and what didn’t;

- Use the insights gained to make necessary improvements to the product, marketing efforts, and customer service.

Launch an MVP in 6 months

With the right development partner, it’s completely achievable. We’ll build your solution from scratch and provide ongoing support after launch.

Let’s talkStep 13. Monitor and measure

How can you tell if an MVP is flourishing and you can move on to developing a complete product? Look for these indicators:

- Increase in your website traffic;

- Positive comments (you have to ask for feedback);

- A steady increase in the number of active users;

- Reducing client acquisition cost (CAC);

- Unchanging or reducing churn rate;

- Increasing number of visitors who convert into paying customers (CR);

- Growing interest from relevant stakeholders (potential partners, media, industry influencers).

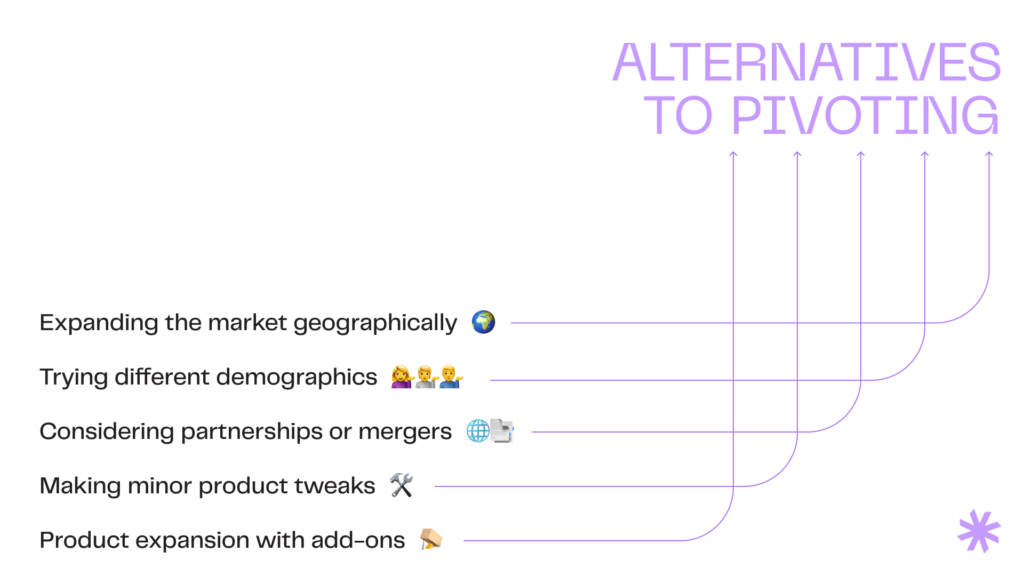

Step 14. Pivot if you must

Sometimes, the initial idea doesn’t work out. In this case, pivoting is essential for survival and growth.

A pivot involves fundamentally changing part of your business model based on feedback and insights gained from your initial operations. This might include changing your product, target market, business approach, or even revenue model to better align with market opportunities and customer needs.

When to pivot?

- Product-market fit isn’t achieved, as shown by poor sales figures, low user engagement, and user feedback;

- Significant shifts in the market, like the recent rise of generative AI, drastically change customer expectations;

- High customer acquisition costs. If acquiring customers consistently costs more than the revenue they generate, a pivot to a new model or market with a better cost-to-benefit ratio may be necessary;

- Scaling challenges. If growth has plateaued or if the business model is too complex or costly to scale effectively, a pivot to a more scalable and manageable model may be required.

How to pivot?

- Decide on the adjustments to be made based on user behavior, market trends, and financial metrics;

- Test before fully committing. Use a prototype or an MVP to validate the new concept without extensive resource investment;

- Plan your finances, as pivoting can strain your resources. Ensure you have enough runway to implement the pivot and achieve new milestones;

- Reflect. Every pivot provides valuable lessons, whether it leads to success or further iteration.

And remember: pivoting is not a sign of failure but a strategic decision. It shows adaptability and responsiveness to the market’s needs.

Being able to pivot effectively can make the difference between a startup’s failure and its long-term success.

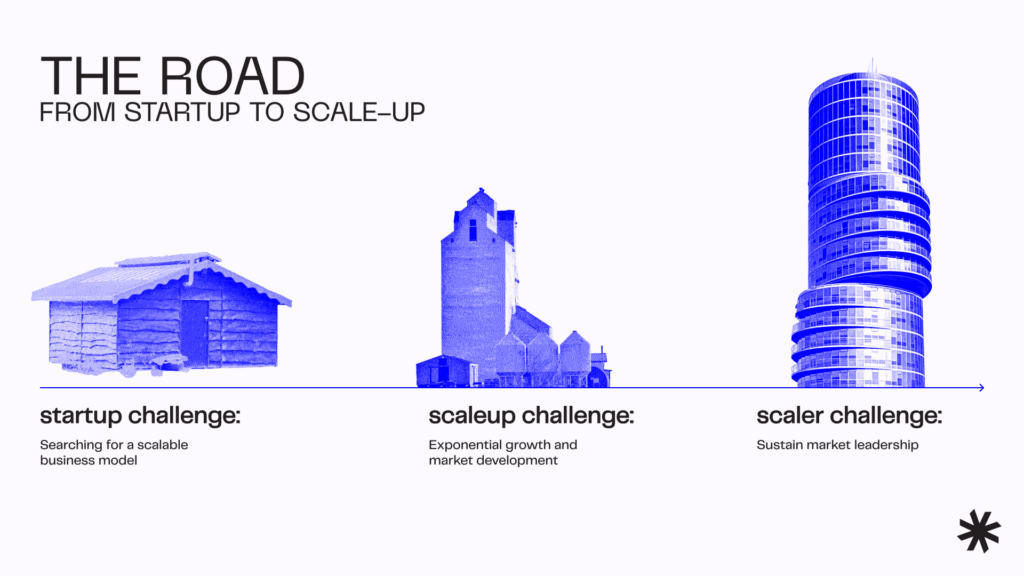

Step 15. Scale and grow your startup

Scaling a startup means increasing its capacity and capabilities. This is done to meet growing customer demand, expand market reach, and manage more complex operations, all while maintaining or improving profitability.

At this stage, a startup moves from being an early-stage entity focused on finding a viable business model to a growth-stage company ready for expansion.

Here’s what typically goes into scaling a startup:

- Enhancing product or service offerings by diversifying their range or improving the quality or functionality of existing offerings based on customer feedback and competitive pressures;

- Market expansion targeting new regions or countries or new customer segments within existing or new markets;

- Operational efficiency improvements through cost/throughput ratio optimization or implementing advanced technologies;

- Securing additional funding through venture capital, loans, or equity funding to support expansion activities;

- Team expansion;

- Strategic partnerships with other companies or even acquisitions to expand product lines, enter new markets, or leverage external expertise;

- Expanding marketing efforts to reach new audiences and reinforce presence in existing markets.

Most big companies were once a startup with a vision. So, don’t hesitate to take the leap! With the right strategies and partnerships, your startup can not only succeed but also become a pivotal player in your industry.

Successful startups that grew to fame

Here are some examples of companies that knew how to build a startup and succeed. They also started as MVPs:

- Instagram started as a location-based social network named Burbn and received its true success after pivoting from the original name and functionality;

- Mailchimp was originally a side project aimed at simplifying access to email marketing tools for small businesses;

- Amazon started as an online bookstore with a simple search engine, an opportunity to review books, and automated email notifications for new books and order-related updates. Its unique feature was a door-to-door delivery and a million-title catalog;

- Airbnb was once a landing page offering nothing more but three airbeds in its creators’ apartment;

- Facebook began as a chatroom for Harvard students;

- Foursquare initially had one feature. It allowed people to check in at different locations and earn badges;

- Groupon spawned from a failed attempt to simplify fundraising. At first, its creators manually reached out to vendors for the deals and only got profit if a certain amount of people purchased.

Challenges startups often face

There are no two identical businesses; hence you will likely encounter unique challenges on your way. However, we’ve collected the top issues most startup founders face and provided ideas on how to create a startup strategy to avoid them altogether.

Lack of demand

The lack of market need buries 35% of new businesses. The primary reason it happens is poor market research, leading to misunderstanding the real market needs. As a result, entrepreneurs build products no one cares about.

But how to create a startup that will get a market share? Unfortunately, finding the right solution may still be hard after establishing the market need. That’s why idea validation is a must-do for startups that want to save money and time. You may start with pre-sales and proceed to MVP development after gaining some traction. Otherwise, iterate and get market feedback until you get a satisfactory result.

Slow growth

Not getting enough customers is often tied to ineffective marketing. Indeed, it’s easy to run out of road chasing trends and spend lots of money without yielding the desired results.

To avoid it, create a marketing plan and learn how to build a startup using low-cost marketing methods and tactics. Next, determine which metrics will provide the most precise picture of your business’s current position regarding your goals.

Inability to scale

Sometimes the revenue grows exponentially, but so do expenses leaving the profit margin stale. It often happens when a business owner rushes startup building and doesn’t plan properly. Another reason is the lack of funding to invest in technology or highly experienced management.

Both can be avoided by taking a steady approach to market research and idea validation. Also, growing a business and fundraising simultaneously is a real challenge. So, you should secure funding before starting the startup development process.

Slow delivery

Failing to deliver a new feature or introduce a new approach by the deadline is a widespread issue, even in established businesses. Ensure you include changes and emergencies in your delivery plan and assign deadlines to every task.

Also, remember that the team is your greatest asset, so take your time to find the right hires. You can also get IT consulting services from an experienced software development company to fill knowledge gaps quickly.

Learn how to reach your business goals more efficiently

Outline your current situation and get a call from a seasoned IT expert with suggestions for improvement

Write usThe cost to build a startup

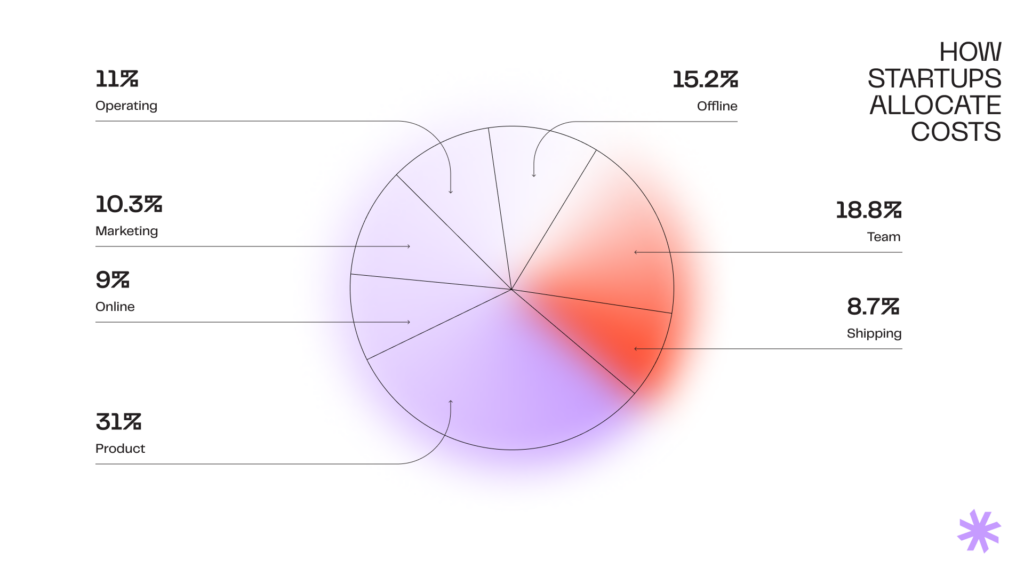

Every type of business has its own financing needs. It’s also worth remembering that you should not just think about how to create a startup company but also how to run and grow it. Each task comes with its own expenses, which we’ll outline below.

First, the costs you’ll incur before you even start a startup include:

- Business registration – $100-$2,000 in Europe and $40-$1,500 or more in the USA;

- Branding – from $0 for a DIY logo using free tools to over $5,000;

- Licenses and permits – from $75-$500 for an online shop to several thousand for a business having physical facilities or manufacturing;

- Insurance – around $65-$200 per month;

- Software (to run a business) – from $25-$500 per month to several thousand if you use custom solutions;

- Equipment and supplies – $1,000-$150,000 or more, depending on the industry;

Costs of running a startup:

- Rent: $0-$50 per square meter per month;

- Employee costs: $0-$50,000 or more per employee per month;

- Taxes: 13-30% from income;

- Marketing: 3-5% of projected gross revenue (recommended);

- Storage and shipping (if applicable): $60-$800 per month or more.

Add up all those costs, and you’ll have the total cost of creating a startup company and running it for one month.

How Syndicode can help build a startup

We are a digital transformation and consulting partner who knows how to build a startup from scratch and enter the market with the right solution at the right time. We have a track record of delivering solutions that have helped our clients become successful startup companies.

Among our latest startup projects is SwiftComply, a B2B city services platform that helps restaurants automate their compliance processes across Ireland and the USA. Since we started working, the company has launched several new services and managed to expand up to 450 cities.

Next is HarvestInn, an MVP of a booking platform for campervan travelers in Australia. The Syndicode team has researched the client’s idea, helped to shape a concept, created a design, and planned the development of a first-mover solution. The platform had over 60 verified hosts offering services one month after launch.

Our other project, Fuzu, gained around 70,000 users the first year after we finished working on it. This job search marketplace collected $6,7M in total funding and kept expanding the range of its services.

Becoming a business owner: summary

Hopefully, this entrepreneur startup guide has given you some ideas on how to build a startup that thrives. In short, the key to starting and maintaining a startup business lies in having the right knowledge. Specifically, you should understand what you want to achieve, where you currently stand, and the steps needed to reach your goal.

The primary condition for success is to offer a solution to a significant problem that people are willing to pay for. We hope that the steps for a startup outlined earlier will help you avoid common mistakes and surround yourself with knowledgeable people.

As an IT consulting and full-cycle delivery company, Syndicode knows how to create a tech startup. We provide the expertise needed to quickly bring your solution to market and ensure its viability. We also offer business analysis, SEO, and marketing services and help businesses automate their processes.

Frequently asked questions

-

Is it possible to launch a startup alone?

Launching a startup alone is definitely possible, and being a solo founder comes with several advantages. For one, it’s often less expensive to start a startup by yourself, you have full control over decisions, and you get to keep all the profits. However, if you wonder how to build a startup solo, we’d say you should prepare for some challenges. First, achieving disruptive growth as a single individual can be daunting. You need to know how to start a startup from scratch, understand your industry thoroughly, monitor your competition closely, market your business, raise funds, and manage a team of freelancers or outsourced specialists, among other tasks.

-

How to ensure startup viability?

To ensure your startup’s viability, focus on creating a solution for a widespread problem that is significant enough for people to be willing to pay for it. Additionally, your solution should be more effective than existing alternatives in the market. Next, determine how to build a startup and raise awareness about your solution among potential customers. Lastly, be responsive to customer feedback and committed to offering high-quality products and services. That’s it.

-

How many startups fail?

About 90% of startups across various industries fail eventually. Among these, 10% do not survive past their first year, and only about 50% make it through the first five years. The primary reasons for failure include a lack of market demand, running out of cash, having a weak team, and an inability to compete effectively. This highlights that it’s not enough to know how to found a startup; maintaining and growing it successfully is where the real challenge lies.

-

How to choose a startup team?

Choosing the right startup team involves preparing for potential challenges and selecting individuals who know how to build a startup. It’s crucial to identify areas where your own skills and knowledge may fall short. Remember, your startup team should be viewed as a long-term investment, ready to support your startup process for years to come. Therefore, it’s important to choose team members who are not only passionate about your vision but whose values align with yours. Additionally, diversity in skills and perspectives is vital. Team members should complement each other’s strengths and weaknesses, promoting an environment where creativity and innovation can thrive. This balance is key to building a successful, cohesive team.

-

How do startups make money?

When deciding how to build a startup, you can choose from various business models, each suited to specific products, markets, and industry dynamics. For instance, startups that produce physical products, provide services or offer one-time purchase software often benefit from a direct sales model. Companies offering software might choose a subscription or freemium model. They can also license their solutions to other businesses. Mobile apps and social media platforms with high traffic typically leverage advertising. Content-based ventures often opt for affiliate marketing to earn revenue. Online marketplaces usually charge transaction fees. Creative projects and startups looking to test the waters before full-scale production may opt for crowdfunding. Finally, innovative tech companies often benefit from government funding, including grants and tax incentives.

-

What’s the difference between a startup and a small business?

The main difference between a startup and a small business lies in the founders’ motives when thinking about “how to build a startup” versus “how to build a small business,” as well as their growth expectations, risk levels, and market approaches. A startup is typically founded with the goal of rapidly scaling. It aims to disrupt existing markets or create new ones. The vision often involves a unique, innovative idea that could significantly change how an industry operates. Startups are expected to scale quickly, target a broad, sometimes global market, and are experimental by nature. This comes with high risk and the potential for high reward. Conversely, a small business is generally established to be profitable and provide a stable income for its owners and employees. Its vision is more localized, focusing on delivering consistent services or products to a community or a specific niche customer base. A small business usually involves lower risk, follows a proven business model such as opening a restaurant, retail store, or consultancy, and grows gradually and linearly, focusing on long-term sustainability rather than rapid expansion.